Not too far off, the first wave of baby boomer will start to retire, and of course that will help fuel Sun Healthcare Group's (NasdaqNM:SUNH) growth in the long term, that in conjunction with the growth in long term care insurance products.

This is a smallcap long term healthcare provider which recently went through a restructure. It seems to have worked because the earnings are growing again. Trading at $8.88, they are currently doing $48 in revenue per share. That means its trading at 0.28 x sales. I think margins should expand as demand for these services grows, allowing SUNH to convert more of that revenue into earnings. The main catalysts for that growth being an older population which now has the means for pay for that care (long term care insurance).

Wednesday, June 28, 2006

Tuesday, June 27, 2006

Semiconductor Slowdown?

It would still be nice to own a stock like FREESCALE (NYSE:FSL). So diversified between the transportation, networking & computer systems and wireless industries. While the rest of the industry is overloaded with inventory, Freescale's inventory levels have been dropping over the past 3 years. Its ROE & ROA is 3x greater the industry average. FSL currently trades at about 13x next years earnings vs 19 for the industry. Its also interesting to note that Freescale has beat earnings estimates every quarter since it came public.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affiliates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affiliates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

Thursday, June 22, 2006

The Cheapest Energy Momo

I like VALERO ENERGY (NYSE:VLO) because its one of the lowest cost refiners, which in a rising oil market will give it a pricing advantage over the competition. This advantage is currently evident using just about any metric.

* Operating margins over the past 12 months increased almost 5% vs 1.8% for the industry.

* ROE of 32.50 vs 11.5 for the industry.

*• EPS growth over the last 5 years is 50% vs 15.59% for the industry.

* Sales growth over the last 5 years of 46.80% vs 15.59% for industry.

* P/E of 8.44 vs 16.10 for industry.

* Trading at 7.5 x cash flow vs 10 for industry.

* Trading at 7.35 this years expected earnings vs 14.21 for industry.

* Trading at 8.38 next years expected earnings vs 13.61 for industry.

Whats interesting is the analyst consensus for next year is less then this year, despite the growth for the industry's estimate. Still, this gives Valero an earnings yield of nearly 12% vs 7.7% for the S&P & 5.2% for the 10-yr t-bond.

This stock is cheap even using the analysts incorrect estimates, and I say incorrect because that estimate will be raised, just like it was by 3% this week, and by 6% over the past 12 weeks vs only .42% for the industry.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affilates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

* Operating margins over the past 12 months increased almost 5% vs 1.8% for the industry.

* ROE of 32.50 vs 11.5 for the industry.

*• EPS growth over the last 5 years is 50% vs 15.59% for the industry.

* Sales growth over the last 5 years of 46.80% vs 15.59% for industry.

* P/E of 8.44 vs 16.10 for industry.

* Trading at 7.5 x cash flow vs 10 for industry.

* Trading at 7.35 this years expected earnings vs 14.21 for industry.

* Trading at 8.38 next years expected earnings vs 13.61 for industry.

Whats interesting is the analyst consensus for next year is less then this year, despite the growth for the industry's estimate. Still, this gives Valero an earnings yield of nearly 12% vs 7.7% for the S&P & 5.2% for the 10-yr t-bond.

This stock is cheap even using the analysts incorrect estimates, and I say incorrect because that estimate will be raised, just like it was by 3% this week, and by 6% over the past 12 weeks vs only .42% for the industry.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affilates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

Tuesday, June 20, 2006

Giving Management Tools

WEBMETHODS INC (NasdaqNM:WEBM) offers SOA (Service-oriented architecture), and BPM (Business Process Management) tools which is used in the planning and integration of Sarbanes-Oxly and Patriot Act compliance into the business processes. Clearly for those reason its obvious why this companies products could be in demand right now.

what is not as obvious is the companies main focus, which is not compliance, but strategic business and IT process modeling, integration and monitoring (then rinse and repeat). With management styles getting more sophisticated (Six Sigma, Performance Management), a pen & pad may no longer cut it, even an excel spreadsheet will get messy.

Usually I would be quick to dismiss such hard to understand business model, but with 1,300 customers, earnings growth and coverage by 11 analysts (which is unusual for a smallcap) I see potential. Mainly the hard to understand business model which seems to have created a mispricing, even with 11 analysts, it has beat estimates the past year. From a growth prospective WebMethods products are in use by several big management teams, and no one wants to leave an edge on the table for the competition.

what is not as obvious is the companies main focus, which is not compliance, but strategic business and IT process modeling, integration and monitoring (then rinse and repeat). With management styles getting more sophisticated (Six Sigma, Performance Management), a pen & pad may no longer cut it, even an excel spreadsheet will get messy.

Usually I would be quick to dismiss such hard to understand business model, but with 1,300 customers, earnings growth and coverage by 11 analysts (which is unusual for a smallcap) I see potential. Mainly the hard to understand business model which seems to have created a mispricing, even with 11 analysts, it has beat estimates the past year. From a growth prospective WebMethods products are in use by several big management teams, and no one wants to leave an edge on the table for the competition.

Thursday, June 15, 2006

PARL revisited using Graham's risk-arbitrage formula

To determine optimal risk/reward in a deal Graham used the following formula:

Annual Return = Probability deal will go through (deal price - current price) / current price

Assuming the going private deal proposed by the CEO has only a 50% chance of working out, the formula for PARL would look like this:

50% ( (29 - 19.50)/19.50 = 24%

If you assume a 25% chance of the deal going through:

25% ( (29 - 19.50)/19.50 = 12%

The yield on the 10-yr is 5.1% and by my estimate the yield for the S&P (based on 2007 estimates) is 7.6%. Compared to the alternatives 12% is a nice return.

Now even if the deal does not go through I believe the downside is very limited. It's currently trading at about 7x next years earnings which is an expected growth rate of 38% this produces a PEG ratio of 0.18, making it one of the cheapest stocks on a growth basis. Its also worth noting that the estimates used are historically conservative because PARLUX continues to beat them quarter after quarter.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affilates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

Annual Return = Probability deal will go through (deal price - current price) / current price

Assuming the going private deal proposed by the CEO has only a 50% chance of working out, the formula for PARL would look like this:

50% ( (29 - 19.50)/19.50 = 24%

If you assume a 25% chance of the deal going through:

25% ( (29 - 19.50)/19.50 = 12%

The yield on the 10-yr is 5.1% and by my estimate the yield for the S&P (based on 2007 estimates) is 7.6%. Compared to the alternatives 12% is a nice return.

Now even if the deal does not go through I believe the downside is very limited. It's currently trading at about 7x next years earnings which is an expected growth rate of 38% this produces a PEG ratio of 0.18, making it one of the cheapest stocks on a growth basis. Its also worth noting that the estimates used are historically conservative because PARLUX continues to beat them quarter after quarter.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. The information above has been obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The author and affilates shall have no obligation to update or amend any information contained above. For informational and educational purposes only.

Tuesday, June 13, 2006

PARLUX undervalued after all

Today PARLUX FRAGRANCES (NasdaqNM:PARL) reported earnings around 2:50pm. The company reported diluted EPS of $0.78 vs $0.71 expected by Wedbush Morgan. The company also reported 82% sales grow over the previous year, contrary to a downgrade note by Wedbush last week which believed sales would decline. I called Wedbush out on this call and took heat for it because after all isn't the job of good analyst to provide insight prior to a market moving event so it's clients can get out before it missed its earnings? Of course it is, but with over 60% of the float short, you have to wonder if the clients were trying to avoid an earnings miss or bank on it?

Apparently the CEO feels the same way. After the close the CEO announced a going private proposal at $29 per share, to eliminate the compliance costs of being a public company and to end disruptions in the company's operations caused by short sellers.

The stock is currently trading at $25.25 in afterhours which is about a 35% premium to the closing price, but is about a 15% discount from the proposed acquisition price.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. Some of the information mentioned is opinion and may differ from fact. For informational and educational purposes only.

Apparently the CEO feels the same way. After the close the CEO announced a going private proposal at $29 per share, to eliminate the compliance costs of being a public company and to end disruptions in the company's operations caused by short sellers.

The stock is currently trading at $25.25 in afterhours which is about a 35% premium to the closing price, but is about a 15% discount from the proposed acquisition price.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. Some of the information mentioned is opinion and may differ from fact. For informational and educational purposes only.

Friday, June 09, 2006

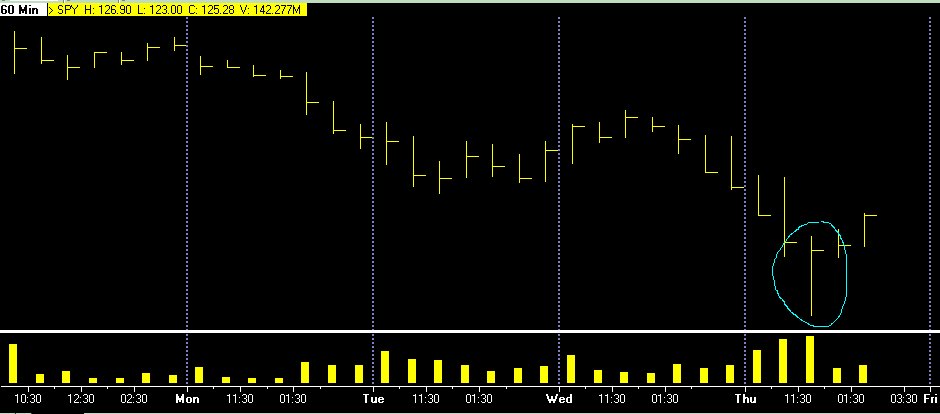

Bottom in place

I have been looking at this market will a bullish bias because I believe stocks are cheap compared to the alternatives. The S&P is expected to earn 95.54 in 2007 according to the bottom-up analyst consensus. This gives the index a yield of 7.7% (95.54/1246) which is almost 3% greater then the 10-yr treasury. Credit spreads and a flat yield curve indicate relatively little risk right now, so for the market to have a 3% risk premium over bonds is just ridiculous. In addition there are more companies beating analyst estimates then not, so the 3% difference may turn out to be understated. In the short term I believe we put in a bottom yesterday because the indices have fallen more then 2 std deviations from their 20 day MA which is normally an aberration and for the hour ending 11:30am we hit a new multi-month low but closed at the highs of that period on a volume spike. Which could very well indicate a bottom in place.

Thursday, June 08, 2006

Irrational Selling?

Parlux Fragrance (PARL) is currently down 13% because of a downgrade by Wedbush Morgan due to poor visibility on their Paris Hilton perfumes. One has to wonder why they would do this the day of the earnings, before the earnings? Why not wait until after the earnings? The whole thing smells wrong on behalf of Wedbush, and this could be a great buying opportunity

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

Wednesday, June 07, 2006

Automating The Financial Planner?

Everyone is now aware of the success of the online brokers. They took the traditional transactional broker, automated him/her which resulted in lower costs and faster executions. Recently I was reminded of how widespread they have gotten when I was pitching a certain someone with $50 million in the market, by the end of my pitch he already bought the idea through his ameritrade account.

The one thing most of these online brokers don't do is financial planning, except for ETRADE. While the others automated the broker, ETRADE automated the financial planner. The brokerage part of the platform allows the user to see how much return they can expect for risk, stress testing (how would the portfolio act on black monday 1987 or 9/11) and performance evaluation with benchmarking. In addition they created a one stop shop for banking, brokerage, credit & lending. This allows them to not only sell on commission but they can also integrate it with the brokerage, so the user can plan out their finances from an investing, banking, spending and borrowing perspective. This allows ETRADE to sell more products such as credit cards and mortgages, and because of the nature of financial planning probably allows them to gather more assets per customer.

Actions are louder then words, and the number are saying the approach is working. Over the past 5 years EPS growth averaged 76% vs 21% for the industry, and valuation wise its cheap trading at 15x this years earnings vs 17x for the industry and 13x next years vs 15x for the industry.

ETRADE may appeal to the retiring baby boomers, but it may really appeal to the younger workforce coming on to replace them, for who it may not make sense to use a traditional financial planner.

The one thing most of these online brokers don't do is financial planning, except for ETRADE. While the others automated the broker, ETRADE automated the financial planner. The brokerage part of the platform allows the user to see how much return they can expect for risk, stress testing (how would the portfolio act on black monday 1987 or 9/11) and performance evaluation with benchmarking. In addition they created a one stop shop for banking, brokerage, credit & lending. This allows them to not only sell on commission but they can also integrate it with the brokerage, so the user can plan out their finances from an investing, banking, spending and borrowing perspective. This allows ETRADE to sell more products such as credit cards and mortgages, and because of the nature of financial planning probably allows them to gather more assets per customer.

Actions are louder then words, and the number are saying the approach is working. Over the past 5 years EPS growth averaged 76% vs 21% for the industry, and valuation wise its cheap trading at 15x this years earnings vs 17x for the industry and 13x next years vs 15x for the industry.

ETRADE may appeal to the retiring baby boomers, but it may really appeal to the younger workforce coming on to replace them, for who it may not make sense to use a traditional financial planner.

Monday, June 05, 2006

Free market hope in Peru

Peru: Alan Garcia claimed victory as Peru's next president with 77% of votes counted and 55% in favor of Alan Garcia and vowed to increase trade ties with the U.S. and challenge Venezuelan President Hugo Chavez's efforts to expand his influence in Latin America.

One stock that will benefit from this is SOUTHERN COPPER CORP (NYSE:PCU). The stock has come under pressure partly due to the threat of a nationalist running who would have taxed Southern Copper's revenue at 3%.

Now that the threat is gone, it presents an opportunity since the stock is almost unchanged today. With over a 10% dividend yield, P/E of 8 and PEG of 0.38, this is cheap stock for income, value or growth investors. With something for everyone, investors from various persuasions can come together and sing kumbaya on this one.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

One stock that will benefit from this is SOUTHERN COPPER CORP (NYSE:PCU). The stock has come under pressure partly due to the threat of a nationalist running who would have taxed Southern Copper's revenue at 3%.

Now that the threat is gone, it presents an opportunity since the stock is almost unchanged today. With over a 10% dividend yield, P/E of 8 and PEG of 0.38, this is cheap stock for income, value or growth investors. With something for everyone, investors from various persuasions can come together and sing kumbaya on this one.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

Sunday, June 04, 2006

Potential for earnings surprises

The summer is generally a slow time. One way to get around that is to play earnings surprises. Below is a list of companies reporting over the next two weeks (06/05 - 06/16) that have a high probability of beating.

VERITAS DGC INC (NYSE:VTS) - reporting 06/06 - This is an oil service company that processes geophysical data on behalf of various energy companies that use the data for oil & natural gas recovery. With the price of energy going up there is demand for oil service companies that help in the energy discovery & recovery processes. That being said I was shocked to find the analyst consensus expects Veritas earnings to decline this year.

COMTECH TELECOM CO (NasdaqNM:CMTL) - Reporting 06/06 - This is a good time to be a wireless technology company, but its especially good when the pentagon has a big demand for your product. On top of its strong organic growth, CMTL is getting bombarded with orders from the pentagon for its warlock jammers which disrupt the electronic signals that Iraqi terrorists transmit to trigger roadside bombs. After the previous sell off the downside is limited while the potential upside is enhanced.

VAIL RESORTS INC (NYSE:MTN) - Reporting 06/07 - Great ski resort and real estate company. This one might sell off on good earnings because they are going into a seasonally slow quarter for them, but that should be used as a buying opportunity because come their normal season it may be much higher.

NOBILITY HOMES INC (NasdaqNM:NOBH) - Reporting 06/08 - This could be an exception to the homebuilder syndrome. They are a Prefab home builder and as result can manufacture homes that are about $30 per sq Ft cheaper.

PARLUX FRAGRANCE (NasdaqNM:PARL) - Reporting 06/08 - This is a perfume company with limited products in a fickle industry, but with 61% of the float short and a PEG of 0.36, the downside could be priced in.

GOLDMAN SACHS GRP (NYSE:GS) - Reporting 6/13 | BEAR STEARNS COS THE (NYSE:BSC) - Reporting 6/14 | A G EDWARDS HOLDING (NYSE:AGE) 6/15 - What can I say? Brokers are hot.

ENTEGRIS INC (NasdaqNM:ENTG) - Reporting 6/16 - Entegris supplies the semiconductor industry with materials and equipment that assure the integrity of the manufacturing process. These days many semiconductor companies are switching to a fabless model, as that trend continues companies like Entergris stands to benefit.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

VERITAS DGC INC (NYSE:VTS) - reporting 06/06 - This is an oil service company that processes geophysical data on behalf of various energy companies that use the data for oil & natural gas recovery. With the price of energy going up there is demand for oil service companies that help in the energy discovery & recovery processes. That being said I was shocked to find the analyst consensus expects Veritas earnings to decline this year.

COMTECH TELECOM CO (NasdaqNM:CMTL) - Reporting 06/06 - This is a good time to be a wireless technology company, but its especially good when the pentagon has a big demand for your product. On top of its strong organic growth, CMTL is getting bombarded with orders from the pentagon for its warlock jammers which disrupt the electronic signals that Iraqi terrorists transmit to trigger roadside bombs. After the previous sell off the downside is limited while the potential upside is enhanced.

VAIL RESORTS INC (NYSE:MTN) - Reporting 06/07 - Great ski resort and real estate company. This one might sell off on good earnings because they are going into a seasonally slow quarter for them, but that should be used as a buying opportunity because come their normal season it may be much higher.

NOBILITY HOMES INC (NasdaqNM:NOBH) - Reporting 06/08 - This could be an exception to the homebuilder syndrome. They are a Prefab home builder and as result can manufacture homes that are about $30 per sq Ft cheaper.

PARLUX FRAGRANCE (NasdaqNM:PARL) - Reporting 06/08 - This is a perfume company with limited products in a fickle industry, but with 61% of the float short and a PEG of 0.36, the downside could be priced in.

GOLDMAN SACHS GRP (NYSE:GS) - Reporting 6/13 | BEAR STEARNS COS THE (NYSE:BSC) - Reporting 6/14 | A G EDWARDS HOLDING (NYSE:AGE) 6/15 - What can I say? Brokers are hot.

ENTEGRIS INC (NasdaqNM:ENTG) - Reporting 6/16 - Entegris supplies the semiconductor industry with materials and equipment that assure the integrity of the manufacturing process. These days many semiconductor companies are switching to a fabless model, as that trend continues companies like Entergris stands to benefit.

DISCLOSURE: I maybe long the stocks mentioned above for myself and clients. Not a recommendation to buy or sell any security. For informational and educational purposes only.

Subscribe to:

Posts (Atom)